Initiating Coverage: United Rentals and Reindustrialist

Benji Rosenblatt

As I cross my five-year mark at Third Prime, I’ve been reflecting on the privilege of being an investor. The job of an investor is deceptively simple: steward capital on behalf of our capital partners (LPs) by finding founder partners who can compound those dollars by building durable and differentiated businesses.

Third Prime’s origin story is unusual by venture standards; we’re outsiders. We didn’t emerge from the Sand Hill diaspora, but instead from the combined experience of white-shoe law firms, Tiger Cub hedge funds, private equity firms founded by ex-Drexel dealmakers, and global investment banks. That heritage shapes everything we do. We build DCFs for pre-seed companies. We follow public businesses that most VCs dismiss as “too boring.” We dial into earnings calls. The through-line is clear. We believe markets are the best classroom, and we like sitting in the front row.

Our rationale is straightforward. To identify greatness, study it. Every week, we meet founders who share their aspirations of “ringing the bell,” because a public listing marks the “ultimate” success in the venture community. Venture investors are good at celebrating the IPO debutantes (CoreWeave, Figma, and the like), but there is as much, if not more, to learn from companies that compounded value for decades without fitting neatly into the venture mold. The operators who built waste management, logistics, and industrial distribution businesses rarely made TechCrunch headlines. They did, however, create immense value for shareholders.

That’s the perspective behind Reindustrialist. This is where I’ll explore lessons from the compounders of the broader capital markets: companies that show what enduring value creation really looks like. The inspiration comes from the original industrialists (Carnegie, Rockefeller, J.P. Morgan, Ford) who deployed capital, ideas, and networks to build the backbone of modern prosperity. As I define it, a Reindustrialist is someone who is applying those same tools today to rebuild and modernize the real economy: how we make things, how we move them, and how we power them.

Enter Reindustrialist

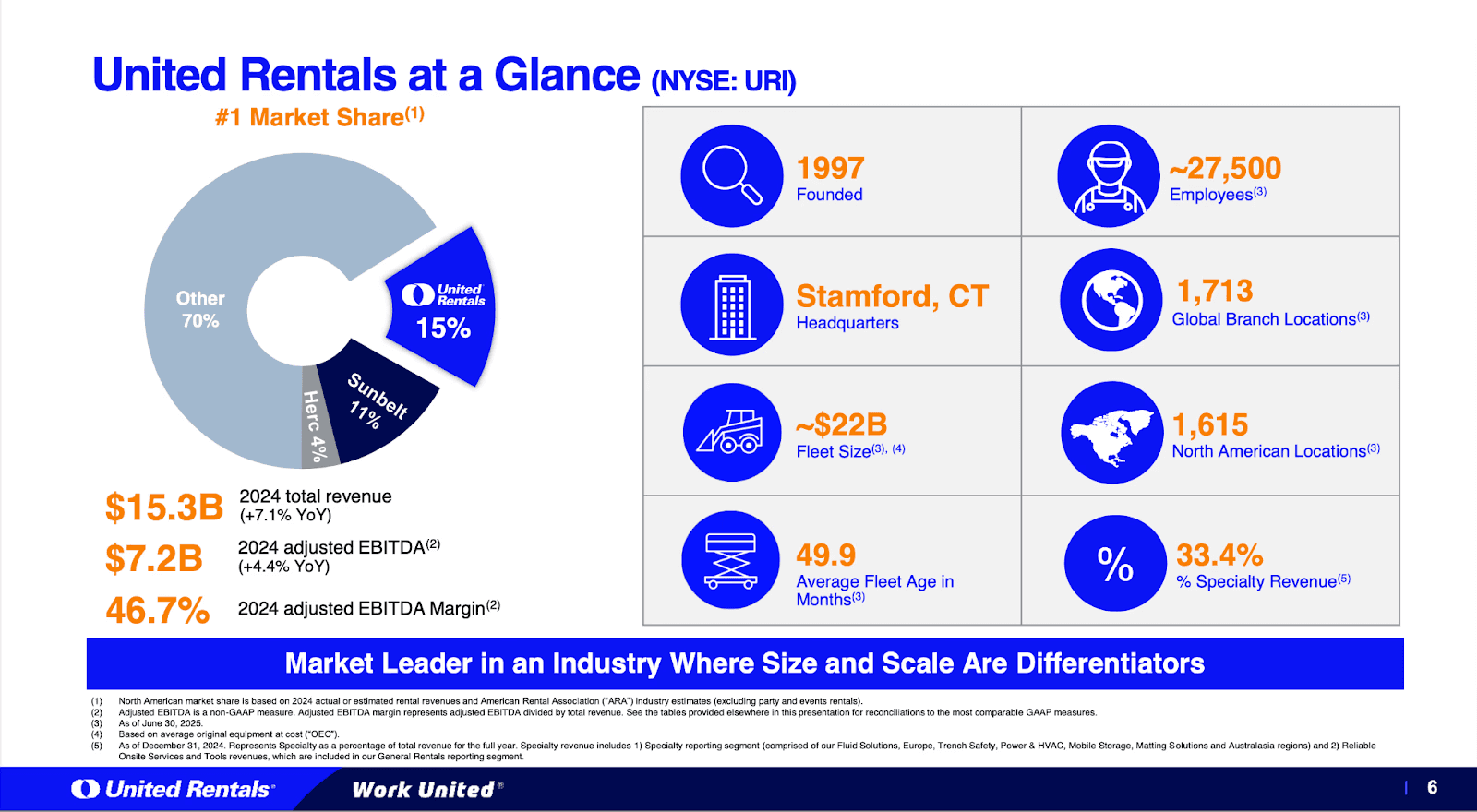

I initiate Reindustrialist with a company unlikely to feature in the tech lexicon: United Rentals (NYSE: URI). Since its 1997 IPO, URI has delivered 40x+ total return and outperformed the S&P 500 meaningfully.

As in any underwriting process, management is central. URI was founded by Brad Jacobs, a serial operator who has built six publicly traded billion-dollar businesses. In his book, How to Make a Few Billion Dollars, Jacobs recalls how Wall Street began referring to him simply as a “Moneymaker.” Rather than reject the label, he embraces it as the byproduct of a repeatable playbook: find a fragmented industry, consolidate it at speed, impose operating discipline, and scale to leadership.

What is United Rentals?

United Rentals is the largest equipment rental company in North America. URI is in the simple business of providing contractors and industrial operators with short- and long-term access to equipment ranging from aerial lifts and power systems to Porta-Potties. Instead of owning fleets outright, customers rely on URI’s scale and logistics network to lower capital intensity and improve project flexibility; think Avis, but the cars are boom lifts, generators, and earthmovers. The model allows customers to consume equipment variably, shifting fixed costs into operating costs.

URI is the kind of business few venture capitalists would touch. As Melius Research highlights in Lessons from the Titans, the model requires heavy CapEx, has limited sources of differentiation, and is at extreme odds with the asset-light models that investors in our business tend to prefer.

That said, the returns speak for themselves. URI, through scale and capital discipline, captured that value in ways its peers could not. How did a company with many attributes investors run from (asset intensity, cyclicality, limited differentiation) become one of the great compounders of modern industrials?

Origins

In September 1997, Brad Jacobs founded United Rentals with the simple thesis that this highly fragmented industry should be consolidated. At the time of incorporation, the market was highly atomized, with 20k+ local operators and the top five players collectively controlling a mere 7-8%. By comparison, it’s about as fragmented as barbershops are today.

In light of this fragmentation, Jacobs saw the opportunity to roll-up mom-and-pop shops into a national platform that could enjoy the benefits of scale in purchasing, fleet utilization, and centralized management.

One of the many lessons Jacobs emphasizes in How to Make a Few Billion Dollars and on the podcast circuit (his Invest Like the Best and David Senra episodes are a must-listen), is the importance of “Getting the Major Trend Right.” In 1997, equipment rental was that trend. Users of heavy equipment were shifting away from owning toward renting, in an effort to reduce capital intensity and improve flexibility. This wasn’t just an idea; there was data to support it. Analysts at the time pegged growth at 15%.

Just as “your margin” was Jeff Bezos’ opportunity, fragmentation was Jacobs’. The rental market’s structure meant a well-capitalized consolidator could quickly gain share. Jacobs and his founding team knew this well. Look back to URI’s S-1, where management clearly outlined that scale advantages were tangible. While synergies are often more optimistic modeling than reality, in equipment rental, the economies of scale, purchasing leverage, and fleet density were undeniable.

Jacobs wasted no time. In URI’s first year, the Company executed dozens of acquisitions. Around the time DLJ initiated coverage, the company had LOIs for 21 targets representing 76 locations, at an average 4.5x EBITDA multiple. Jacobs’ strategy was centered around multiple arbitrage and cost savings to further amplify the accretion of these acquisitions.

The boldest move came in June 1998, when URI acquired U.S. Rentals for ~$1.2bn. The deal catapulted URI to ~7% market share and $1.4bn in revenue, transforming it overnight into a national player and providing the platform for 200+ acquisitions over the next five years.

Investors were divided: could URI turn what was widely considered a “shitty industry” into a durable, profitable compounder? Or would the Company collapse from debt, botched integrations, and cyclicality?

By 2005, URI was the largest player in the industry, generating >$2.5bn in revenue. But the capital structure was stretched, integration risk remained high, and EBITDA margins lagged best-in-class peers. Was URI just an overlevered roll-up bound to fail, or were they building a scalable platform?

From Roll-Up to Real Company

To execute a roll-up well, you need several key ingredients:

A systematic sourcing engine to identify and acquire targets

Valuation discipline to only pursue accretive deals

A repeatable playbook to integrate assets and realize synergies

A thoughtful capital structure to balance growth and leverage

Cultural alignment and incentives to convert a portfolio of acquisitions into a unified company

By the mid-2000s, URI had demonstrated 99th-percentile ability in sourcing and valuation discipline. The Company could find and close deals at pace (averaging one every couple of weeks), and it enjoyed the benefits of scale in purchasing and geographic coverage. Integration efforts and cultural alignment, however, lagged badly. As you may expect with this frenetic of an acquisition rate, URI still looked like a collection of disparate businesses. Each branch operated with its own systems, processes, and even customer relationships. The benefits of size were real, but they had yet to build the backbone of a unified enterprise.

Even the best compounders encounter turbulence, and URI was no exception. By 2007, despite strong top-line growth and market leadership, the Company clearly was not integrated. In light of these challenges, the board determined it had a fiduciary responsibility to explore a sale, believing a new owner might make the tough changes needed to unlock URI’s full potential.

Shortly thereafter, URI received a $6.6bn offer from Cerberus (including the assumption of debt). The onset of the Global Financial Crisis derailed the transaction, with Cerberus choosing to walk away, paying a $100mm breakup fee in favor of closing.

The following 18 months became existential. With heavy leverage and direct exposure to U.S. construction, the investment community widely expected URI to collapse into bankruptcy. Management took extreme measures to survive, like selling off parts of the fleet at distressed prices to raise cash, slashing capital expenditures, and cutting costs aggressively, all in the pursuit of deleveraging. These moves were defensive, but they kept URI solvent long enough to fight another day.

URI experienced many growing pains, but one was particularly exacerbated by the recession: a broken incentive structure. The Company compensated branch managers solely on EBITDA growth, with no costs associated with accumulating a disproportionately large fleet. This structure incentivized counterproductive behavior, with branch managers holding on to idle equipment instead of sharing it with neighboring branches out of fear that sharing would hinder their ability to expand EBITDA. To solve this, the Company introduced a new metric, “Return on Controllable Assets.” The metric incorporated fleet costs into bonus calculations and compensated managers for how well they utilized assets, in addition to reframing compensation from branch-level to district-level, so branches were economically incentivized to cooperate.

As branches locked arms and operated in a more unified manner, the Company directed focus upmarket to higher-quality customers, as many smaller players showed weakness and even closed in the wake of the financial crisis.

During this time, United Rentals launched its “National Accounts” strategy, providing a higher level of service to large customers that rented more than $500k in equipment per year. These customers enjoyed a single master contract with consistent rates and terms across regions, centralized billing and credit, dedicated account managers, and a unified tech experience via the Company’s “Total Control” dashboard. In addition to providing customers with insight and visibility into their rented equipment, URI was known to notify customers when they were paying for equipment they weren’t using, a clear example of their long-term approach toward customer relationships.

As URI moved upmarket, revenue became stickier, utilization rose, pricing became more rational and scientific, credit risk subsided, and this cohort became a prime target for cross-selling.

As these changes began to permeate through the organization and the Company regained its footing, it came back boldly. To further consolidate its leadership, URI acquired RSC Holdings, then the #2 rental company in North America, and URI’s fiercest rival in the large account segment.

The RSC acquisition marked a strategic inflection point for United Rentals. The combined platform had $7bn in fleet value and $4bn in revenue, but more importantly, it rebalanced the business. RSC’s heavy industrial mix complemented URI’s construction exposure well, broadening the customer base and reducing cyclicality, a key priority for the business that has remained in place for the last decade.

The combination naturally strengthened purchasing leverage, fleet utilization, but more importantly, cemented URI as the supplier of choice for “National Accounts” across both industrial and infrastructure markets. The merger transformed URI from a leveraged roll-up into a diversified, cycle-resilient industrial compounder.

From Acquirer to Compounder

The period after RSC marked the end of URI’s roll-up era. The playbook shifted from buying growth to earning it through pricing analytics, centralized systems, and a relentless focus on return on capital. A decade earlier, URI was a patchwork of rental yards held together by spreadsheets; by 2015, it operated as a unified industrial platform.

With the advantages of scale already realized, the Company pivoted its M&A strategy exclusively to high-return opportunities during the next 8 years, prioritizing specialty rental verticals and strategic regional acquisitions instead of the frenetic deal pace of the prior decade.

At URI’s most recent investor day in 2023, the Company shared its 2028 targets, which reflect sizable shifts in business mix toward specialty rental segments in pursuit of higher margins and less cyclicality.

Specialty categories include Power & HVAC, Trench Safety, Fluid Solutions, Tool Solutions, and Modular Space and Storage. These segments typically generate superior margins, require less capital investment, and have more stable demand profiles due to the broad swath of customer end markets (industrial maintenance, infrastructure, utilities, and emergency response) outside of traditional construction. As specialty rentals become a bigger share of overall revenue, margins expand, and volatility dampens, enabling the Company to compound earnings and free cash flow through the cycle.

Since specialty rentals have grown from 7% to 35% of revenue in the past dozen years, the Company’s financial profile has transformed. URI’s general and specialty rental businesses have proven symbiotic, as the Company has been a massive beneficiary of cross-selling between these two segments. This has resulted in a more diversified, cycle-resilient platform where customers can source everything from one national supplier. No competitor can replicate that at scale.

Despite being in the equipment rental space, URI differentiated itself through continued technology investment. The Company launched a cloud-based platform that helps customers right-size fleets, digitally book pickup or service requests, and analyze usage through data. In an industry long resistant to technology, URI has demonstrated that digital transformation can become a durable source of competitive advantage.

Relevance to Venture

As AI-enabled roll-ups expand in mind- and wallet-share, URI provides a playbook for founders and investors working to rebuild the real economy.

Operational excellence is the real moat: On their face, roll-ups sound easy. “Slap technology on a functioning business, optimize sales, cut costs, and reap the rewards.” This simple framing overlooks the truth that delivering the core product or service well wildly eclipses the perceived ease of this playbook. In URI’s case, it wasn’t scale alone that led to the Company’s success; it was systems. Once the business had discipline, it started to compound. The same holds true for all of venture: execution supersedes vision. I believe that founders who institutionalize excellence early go on to build companies that compound by design, not by luck.

Customer focus compounds: URI didn’t just chase volume; it chased the right customer. By moving up market and serving “National Accounts”, the Company benefited from customers that valued uptime, service, and convenience, and built relationships with customers willing to pay a premium for reliability and breadth. Its “one-stop shop” model turned equipment rental into partnership, not procurement. It’s important to find customers who feel the value you create, not just the price you charge; durable relationships make for durable businesses.

Integration > acquisition: The past few years have seen a surge of venture-backed roll-ups. Despite the increase in activity, if United Rentals teaches anything, it’s that the hard part isn’t buying assets; it’s integrating them. URI spent its early years acquiring assets more quickly than it could unify them, eventually discovering that scale without systems breeds fragility. As the Company shifted focus from deal velocity to integration, the compounding began. For founders taking the platform path, it’s important to realize speed may result in headlines, but integration will drive returns.

Incentives shape outcomes: URI is a great case study in the impact of incentives. In the early days, when branch managers were paid based on their location’s EBITDA, they hoarded assets instead of optimizing company-wide economics. When the Company shifted to Return on Controllable Assets, the culture changed, as did the economics. Startups must constantly re-evaluate incentives at each phase of growth; what works for ten people can misfire for one hundred. The most effective leaders revisit incentive design and tune it to promote collaboration, capital efficiency, and long-term value creation.

If you see opportunity where others see fragmentation or indifference, I’d love to connect. We’re eager to partner with founders who want to build the next great compounder.

Research Archive

Reindustrialist: Upcoming Coverage

Upcoming

Join the research distribution

© Reindustrialist 2026. All rights reserved.

The information provided is for informational purposes only and does not constitute investment advice.